In 2025, cross-border business was no longer as easy to do. This was almost a shared feeling among all e-commerce platforms and sellers.

If you had to sum up the global cross-border e-commerce industry in 2025 in one sentence, it would undoubtedly be: “endless setbacks and troubles from within and without.”

In 2025, the United States’ repeated tariff shocks, another contraction in global consumer spending, and structurally elevated traffic-acquisition costs in the North American market—these weighed on every cross-border e-commerce practitioner with unprecedented force.

The information-gap dividend that had fueled growth over the past decade was wiped out, and supply-chain advantages were flattened as products became extremely homogenized.

Looking back at 2025, cross-border e-commerce moved from “wild growth” to “meticulous cultivation.” As the curtain rose on 2026, cross-border practitioners were confronted with structural problems this year and beyond: when global expansion slows, white-label profits are depleted, the fight for traffic hits its ceiling, and efficiency runs into bottlenecks, how can cross-border e-commerce find a new map and new weapons?

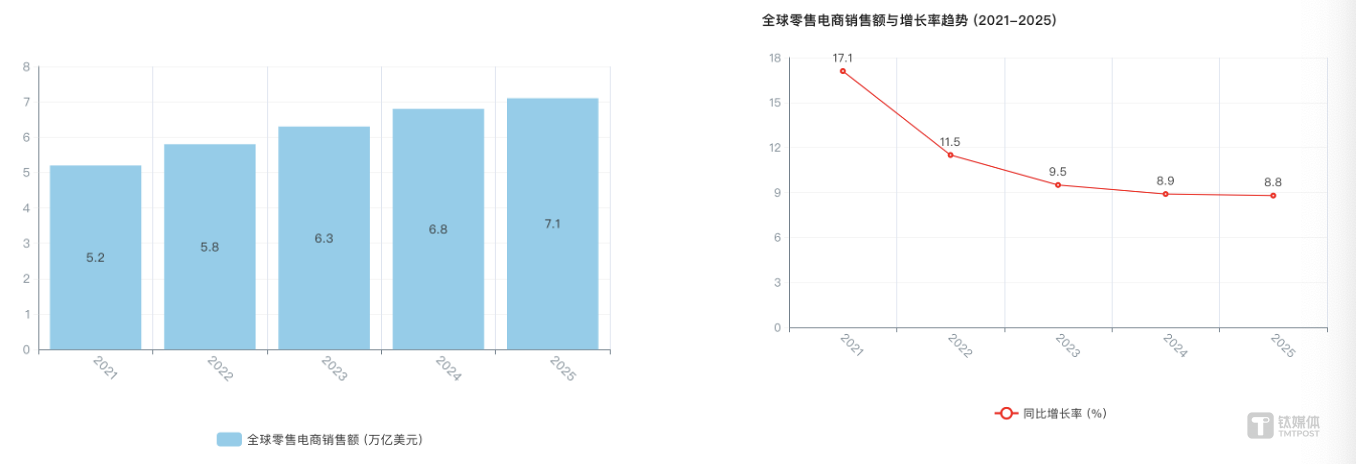

Looking back at global e-commerce growth data over the past five years, a clear deceleration curve emerged.

From the 17.1% global online-shopping boom in 2021, to the landmark inflection point in 2023 when it fell below 10% for the first time, and to 2025 settling at a single-digit “new normal” of 8.8%, it’s not hard to see that the era when you could grow easily just by riding a rising market has gone for good.

Trend chart of global retail e-commerce sales growth rates, 2021–2025 (Table 1 + Table 2) | Graphic: Chuhai Cankao

Trend chart of global retail e-commerce sales growth rates, 2021–2025 (Table 1 + Table 2) | Graphic: Chuhai Cankao

A contraction in global consumer spending was the most important macro backdrop behind the slowdown in growth. In 2022–2023, inflation in key e-commerce markets such as Europe and the United States once topped 9% (hitting 9.1% in the U.S. in June 2022 and 10.6% in the eurozone in October 2022). Although it gradually fell back to the 2–3% range in 2024–2025, the sharp hit to households’ real purchasing power was difficult to reverse—especially amid the headwinds from tariffs.

Tariff policy swings in 2025 were undoubtedly a major factor behind weak e-commerce growth. As the U.S. continued to impose additional tariffs on China, the overall tariff rate on Chinese goods exported to the U.S. rose. For major cross-border e-commerce categories such as apparel and electronics, tariff rates generally sat in the 15–30% range, and even reached as high as 45% for some products. Tariff costs were passed through the supply chain, and in the end the added burden from tariff fluctuations still had to be absorbed jointly by platforms, sellers, and end consumers.

Year-by-year increases in global online customer acquisition costs also made conversion harder and dragged down growth. According to third-party data, CPM on Meta’s social platform Instagram in the U.S. reached $9.17 in Q4 2024, while Facebook’s CPM was $8.66 over the same period; Instagram’s CPM was expected to rise further to $10.48 by Q4 2025. Meanwhile, the average CPC on Amazon’s U.S. marketplace climbed from $0.84 in 2024 to around $1.12 in 2025, and some highly competitive keywords exceeded $2 in 2025. Higher ad costs reflected both intensifying competition among sellers and platforms’ deliberate efforts to screen and filter merchants.

A combination of these factors kept global e-commerce sales growth hovering around the 8.8% baseline, and posed the same question to every player: under this triangle of pressures, where will growth come from?

A tale of two worlds

Even as global e-commerce growth slowed, the wave of Chinese companies going global created a “tale of two worlds” dynamic, with global e-commerce platforms showing sharply divergent growth trajectories.

The “ice” side is that growth at mature giants such as Amazon and eBay has already trended toward the single digits. Take Amazon as an example: the growth rate of its e-commerce business fell from over 35% at the peak of the pandemic to the current 10.6%, signaling that its strategic focus has shifted from outward “land-grabbing” expansion to inward “deep cultivation and efficiency gains.”

The “fire” side is the breakneck surge of emerging players such as PDD’s overseas app Temu, SHEIN, AliExpress, and TikTok Shop. Earnings data show that Shopee was still maintaining rapid growth of around 30%, while the bigger variables—Temu and TikTok Shop—were estimated by multiple third-party research firms to still be growing at extremely high double-digit or even triple-digit rates, acting as “catfish” that keep the market on edge.

This conflicting picture—between industry growth and platform growth, and among platforms themselves—laid bare a stark reality for the cross-border sector in 2025: it wasn’t growth itself that slowed, but the"extensive, homogenized"growth model of the past decade. The old playbook no longer worked; strategies that relied purely on buying traffic and moving supply chains had already run out of steam.

Competition in cross-border e-commerce has moved from an era of rising tides and expanding increments into a phase of zero-sum competition that tests platforms’ overall operating efficiency, ability to innovate business models, and strategic staying power.

From global expansion to regional focus

In step with the slowdown in overall growth, cross-border e-commerce platforms in 2025 almost without exception gradually eased off on launching new sites, shifting instead to differentiated, intensive cultivation of their strongest regions.

In the past, Shopee tried to expand into Europe, but it has since shifted its strategy to Latin America while consolidating its foothold in Southeast Asia. Temu’s development approach, in particular, reflected a broader shift among cross-border platforms—from broad, blanket expansion to deeper regional cultivation.

Temu launched operations in more than 40 markets worldwide in 2023; by the end of 2024, its global footprint had grown to more than 80 markets. In 2025, Temu opened only 10 major new markets—including Colombia, the UAE, Slovakia, and Bulgaria—while doubling down on localization and vigorously promoting the local-to-local model. Amazon, AliExpress, and eBay had long since entered a mature, incremental-operations phase and opened no new markets in 2025.

This shows that platforms have effectively reframed the question from “Where should we go?” to “Where should we go deeper?” They are no longer pursuing a pepper-sprinkling, all-fronts offensive; instead, they are concentrating resources on fortifying and deepening the moat in their strongest markets, while cautiously scouting for a second growth curve.

Reducing reliance on the U.S. as a single market became the top keyword in 2025 for cross-border platforms like Temu and Shein—platforms that primarily depended on the small-parcel cross-border model and focused heavily on the U.S. market. After the White House began scrapping the de minimis duty exemption for low-value parcels in February 2025, a tariff-and-trade war that lasted for nearly a full year got underway, pushing platforms and merchants to accelerate an “U.S. + N” footprint.

According to available data, in the first two weeks of Temu’s second quarter of 2025 (March 31–April 13), its average daily ad spend on platforms such as Meta, X, and YouTube in the United States was cut by 31% compared with March. Starting April 9, it halted all advertising placements on Google Shopping. By contrast, Temu’s April spending in the UK and France rose 40% and 20% month over month, respectively, signaling a heavier bet on Europe.

Along the same lines, finding growth in emerging markets became another key phrase for all platforms in 2025. Developed markets such as Europe, Australia, and Japan, as well as emerging markets such as Brazil and Mexico, became the most frequently cited targets across the board.

In Brazil—a market many platforms were betting on—Amazon still put infrastructure first: in 2025 it added more than 100 new fulfillment/delivery centers and rolled out same-day and one-hour delivery services in São Paulo and Rio de Janeiro. Shopee, meanwhile, completed 13 large-scale fulfillment centers and 180 logistics hubs in Brazil in 2025, achieving next-day delivery for 25% of orders in the São Paulo metropolitan area. At the same time, it surpassed 3 million local sellers, moving further toward deep localization. More importantly, Shopee exited Latin American markets such as Colombia and Chile in Q4 and concentrated its resources on Brazil.

What Shopee’s move shows is that doubling down on advantaged markets became the tactical choice for cross-border platforms after they narrowed their regional focus in 2025.

Alibaba’s AliExpress treated South Korea as a key stop in its regional deepening strategy. After years of sustained build-out, AliExpress expanded local warehousing in 2025 and increased capacity at its South Korea-bound warehouse in Weihai, Shandong. By combining its “Choice channel + managed fulfillment + local warehouses,” it offered Korean consumers high value-for-money products and fast 3–5-day delivery, prying open a gap in the heartland of local giants such as Coupang—one of its most representative regional breakthrough cases in 2025.

Even in Southeast Asia, a market where e-commerce platforms have already fought fierce battles, there is still enormous room to be unlocked. Although Shopee and TikTok Shop had largely secured the top-two positions in the region, Southeast Asia’s e-commerce ceiling was still far from in sight, and the market continued to show strong growth momentum.

Take TikTok as an example: in 2025, TikTok Shop’s annual cross-border e-commerce GMV in Southeast Asia more than doubled year over year; average daily GMV rose 90% YoY; and by year-end, the peak single-day transaction volume was nearly twice that of late 2024. During the “Double 12” campaign, TikTok Shop’s cross-border e-commerce GMV surged 2.7x YoY, with short-video-driven GMV jumping 257%.

To some extent, these growth figures show that in an e-commerce era fueled by high traffic, high-quality content remains one of the best ways to acquire traffic. TikTok Shop used short-form video to create a new “shelf,” enabling consumers to move naturally from discovery to purchase while consuming content, triggering unplanned spending and opening up new dimensions of consumption. Amid homogenized competition—where everyone is fighting on traffic and supply chains—it carved out a highly differentiated path to growth.

From mass listings to taking brands global

If regional focus marked the new battle lines drawn by major platforms in 2025, then upgrading from mass listings to branding became the shared consensus among everyone on the battlefield.

In this wave of brand upgrading, cross-border e-commerce platforms showed unprecedented resolve and boldness—even going so far as to turn the blade inward and accept short-term pain at the cost of short-term gains.

Take Amazon as an example: in 2025, Amazon once again tightened its brand management requirements. It not only demanded more comprehensive brand documentation and product traceability systems, but also introduced a Brand Health Rating system that set explicit expectations for the quality of merchants’ brand operations—pushing sellers toward long-term, sustained brand management.

Higher requirements for merchants’ brands, operations, and capital raised the bar for entering Amazon. According to a Marketplace Pulse report, Amazon added 165,000 new sellers in 2025, down 44% year on year, and the number of active sellers fell by about 31% from 2021 to 2025.

SHEIN’s branding strategy, by contrast, was implemented through offline experience stores and opening up to third-party sellers. Offline experiential retail brings shoppers closer to SHEIN, while SHEIN also leveraged its platform traffic to help more branded merchants expand overseas. In September 2025, SHEIN launched the “SHEIN Xcelerator” brand incubation and support program, aimed at emerging and established brands worldwide—including Chinese designers and brands—providing incubation and support for global growth.

AliExpress likewise pushed an aggressive branding strategy. On the one hand, the platform drew overseas consumer attention by signing celebrities such as David Beckham, Korean star Ma Dong-seok, and Saudi footballer Salem Al-Dawsari. On the other hand, through initiatives such as the “Super Brand Global Expansion Program,” it recruited well-known brands from platforms including Tmall and Amazon, and joined hands with prominent Chinese brands such as HONOR, Baseus, and Nubia to expand incremental growth in overseas markets.

This combination of moves helped AliExpress rank among the top 10 comprehensive platforms by growth across multiple developed-country markets. In the U.S. in particular, AliExpress’s website visits grew 18.7% year on year for the full year of 2025.

Even more notably, Southeast Asia—once widely seen as a low-price, unbranded market—was also undergoing a branding upgrade.

Recently, TikTok Shop released a set of figures showing that GMV growth across TikTok Shop Southeast Asia’s core cross-border e-commerce categories all exceeded 120%. Among them, the computers and office equipment category saw year-on-year GMV growth of nearly fivefold; categories such as beauty appliances, mother-and-baby products, and health supplements all grew by more than threefold; and regionally distinctive categories including home and household textiles, pet supplies, and Muslim fashion likewise achieved more than threefold growth. All of these high-growth categories are tracks that place a premium on product quality, user experience, and brand positioning.

As platforms proactively “take a hit” and reshape the ecosystem with compliance and branding as their shield, sellers’ survival logic is being rebuilt in lockstep——the room left for product-spraying sellers has been sharply squeezed, while companies that truly have brand DNA have instead gained valuation premiums and a window to go public amid a broader slowdown in growth. This structural divergence became the most telling market signal for cross-border merchants in 2025.

On the one hand, product-spraying sellers have been exiting one after another. Today, cross-border platforms’ traffic-allocation mechanisms have tilted toward brand sellers, and the era of “traffic dividends” for product-spraying sellers is all but over. According to a 2025 survey by AMZ123, more than 60% of small and midsize sellers saw net profit decline in 2025, with 31% down by more than 50%; some sellers mentioned exiting or pivoting.

On the other hand, capital markets are incentivizing brand sellers to go global. A representative case is Insta360 (Insta360 Innovation): since it went public in June 2025, the company’s market capitalization at one point reached 100 billion yuan on the back of the Insta360 brand’s standout global performance. More recently, xTool, Roborock, Taili Technology, and WOOK (WOOK Feifan), among other brand-led cross-border merchants, have successively submitted prospectuses to the Hong Kong Stock Exchange, awaiting positive market feedback.

WOOK (WOOK Feifan), a consumer electronics brand that started in Indonesia, has moved away from the “white-label, product-spraying” model. By building three major in-house brands—VIVAN, ROBOT, and SAMONO—it has earned positive market reception. Its prospectus shows that in the first three quarters of 2025, it recorded revenue of 880 million yuan and adjusted net profit of 62 million yuan.

Logistics and AI

If brand is the magnet that draws users in, then an efficient, reliable service ecosystem is the moat that keeps them and enables long-term profitability. As a result, platform competition has extended into an all-chain infrastructure contest spanning logistics, payments, platform technology, and more.

Logistics, as the “last mile” connecting goods and consumers, is the most central—and most cash-intensive—battleground in this ecosystem race. How much a platform invests largely determines how high its competitive barriers can be.

Amazon is a pioneer in infrastructure buildouts. To keep improving its fulfillment capabilities, it has continued investing in logistics infrastructure worldwide, with cumulative investment to date topping US$100 billion. In 2025, Amazon Global Logistics (AGL) added six pickup cities in China, launched a new ocean shipping route from Vietnam to the United States, and opened its first Amazon Global Smart Hub Warehouse (GWD) in Shenzhen toward year-end. These major investments translated into an outstanding fulfillment experience, so while other parcels were still crossing the ocean, Amazon Prime members were already receiving their purchases with same-day or next-day delivery.

Within Alibaba International Digital Commerce’s footprint, Cainiao Group—responsible for logistics—first opened a Hong Kong supply chain center in 2025, enabling a “stock in Hong Kong, ship worldwide” logistics model and shortening AliExpress sellers’ stock-prep lead time from 7–10 days to 3–5 days; it also took 100% control of 4PX, integrating its overseas warehouse network and standardized smart logistics solutions to strengthen AliExpress’s competitive edge in cross-border delivery speed and user experience.

Platforms such as SHEIN and Temu, meanwhile, strengthened localization and local-fulfillment models to make up for the limitations of a single cross-border small-parcel approach. SHEIN, in particular, built out local supply chains to hedge the risks of relying on a single supply base. Starting in 2023, SHEIN began working with local suppliers in Brazil and has since established partnerships with 2,000 apparel and textile factories there.

Beyond logistics and supply chains, cross-border e-commerce has also tried to ignite an AI evolution war—upgrading AI from a “nice-to-have” tool into a foundational “operating system” that rewrites the industry’s rules—not only improving operating efficiency through AI, but also aiming to trigger cascading change across three major dimensions: consumer experience, supply–demand matching, and business decision-making, pushing the industry’s shift from traffic-driven growth to intelligence-driven growth.

In this race to retool for intelligence, nearly every player has already joined. Amazon is leveraging its technology base, vast consumer data, and AWS cloud services to continuously optimize intelligent scheduling for its FBA warehousing and roll out AI tools for merchant operations; TikTok, with algorithms in its DNA, has deeply embedded AIGC into its content creation and distribution system; and SHEIN—known for its “small-batch, fast-turn” model—has long been applying AI at scale across areas such as trend forecasting, demand planning, and automated review of product listings.

In the practice of using AI to cut costs and boost efficiency, Alibaba International Digital Commerce Group (AIDC) is also a path worth watching. Building on a light-asset, scenario-driven approach, AliExpress has continuously rolled out a suite of tools—AI translation, AI product selection, AI customer service, AI marketing, and more. Powered by these tools, small and medium-sized merchants can gain big-seller capabilities without having to build large in-house teams. Meanwhile, Alibaba.com, which focuses on wholesale, kept upgrading its AI Business Assistant throughout 2025 and released the agent-based AI Mode to buyers worldwide, helping SMEs around the globe fully automate cross-border e-commerce procurement workflows.

This model of empowering merchants rather than replacing them enabled AIDC to grow revenue by 10% in the third quarter of 2025, while also achieving adjusted quarterly EBITA profitability for the first time.

AI is not merely synonymous with “burning cash.” By improving merchants’ efficiency, it has delivered a win-win for both platforms and merchants.

2026, a year to put down roots and grow

Looking back at 2025 from the threshold of 2026, the “dividend hunting” model in cross-border e-commerce has come to an end, and global e-commerce has entered an “era of resilience.”

The strategic pivots of leading players have already set new bearings for the industry. Competition going forward will be a comprehensive contest of logistics infrastructure, supply-chain efficiency, brand strength, and the level of intelligence. Deep regional cultivation will define the boundaries of the main battlefield ahead; branding will be a higher-dimensional weapon for future competition; and logistics and AI will be the foundational bedrock for building a defensible moat.

There may be fewer get-rich-overnight myths in the future, but there will be more stories of businesses taking root and growing steadily. After all, leaving the wild frontier behind is not the finish line—it is the true starting point of an era of meticulous cultivation and sustained returns. (Authors | Wang Lu, Yang Xiujuan, Luo Wenqin, Editor | Luo Wenqin)