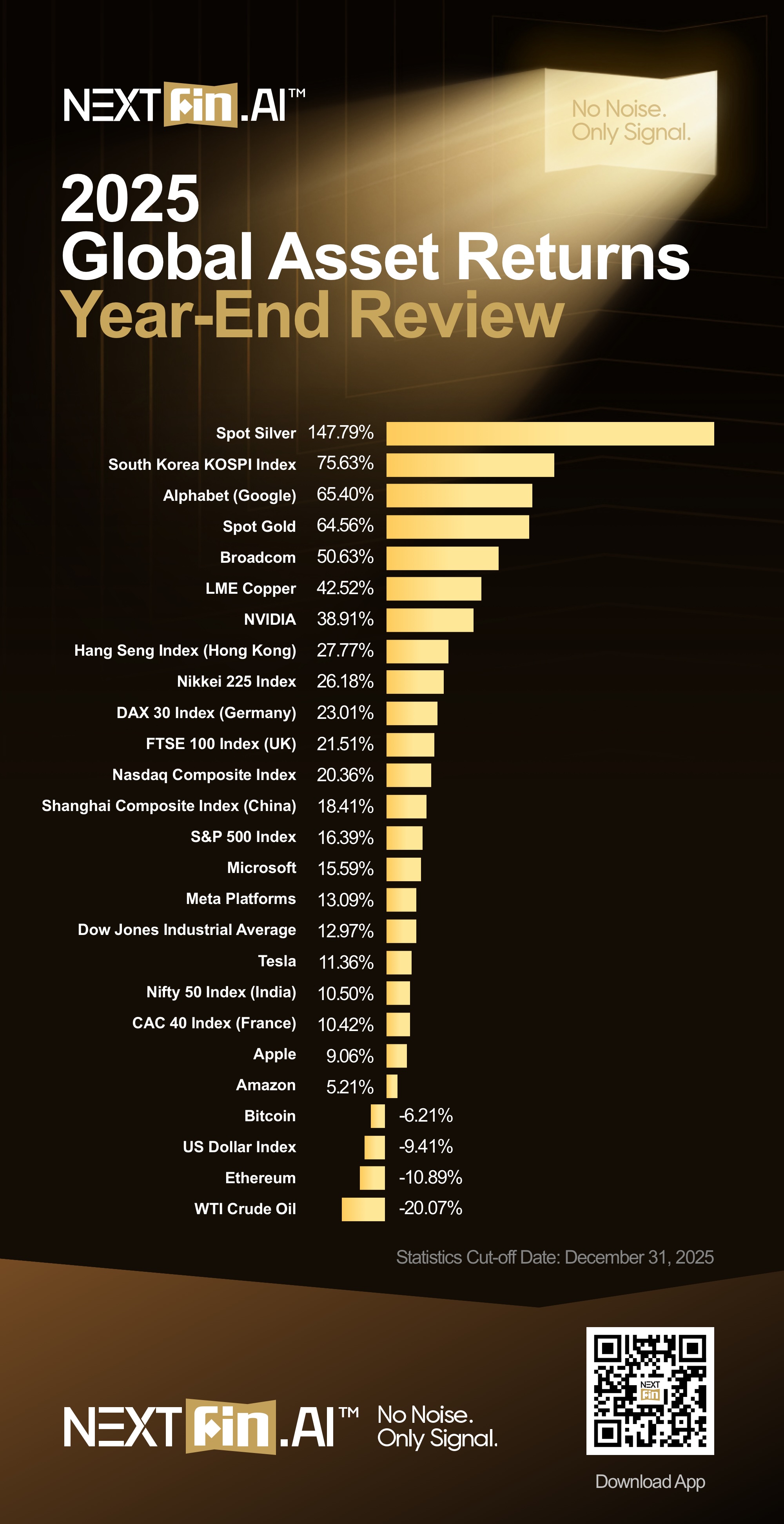

NextFin News - The global asset landscape in 2025 witnessed a remarkable and varied performance pattern, marked by extraordinary gains in precious metals and robust equity rallies across Asia and the United States. According to data as of December 31, 2025, spot silver led all asset classes with a staggering return of 147.79%, followed by the South Korean KOSPI Index which soared 75.63%. Notably, tech giants Alphabet (Google) and Microsoft posted gains above 15%, reflecting the sustained momentum in technology sectors fueled by AI innovation. Spot gold appreciated 64.56%, underscoring its renewed status as a safe haven amid geopolitical tensions. Meanwhile, traditional benchmarks such as the S&P 500 and Dow Jones Industrial Average recorded solid returns of 16.39% and 12.97% respectively, corroborating sustained US market resilience.

Conversely, certain asset classes faced headwinds: Bitcoin and Ethereum declined by 6.21% and 10.89% respectively. The US Dollar Index weakened 9.41%, and WTI Crude Oil plummeted by over 20%. These downturns reflect complex macroeconomic shifts, including monetary easing from major central banks and geopolitical developments affecting commodity markets. Globally, stock markets outside the US also performed well with the Hang Seng, Nikkei 225, DAX 30, and FTSE 100 all delivering double-digit returns, while India’s Nifty 50 Index rose 10.50%.

The surge in silver and gold was propelled by a mix of strong industrial demand, particularly in electronics and renewable energy applications, and intensified investor flight to safety amidst ongoing geopolitical risks in regions including Ukraine and the Middle East. This safe haven demand was amplified by global monetary policies that saw multiple interest rate cuts, reducing opportunity costs of holding non-yielding precious metals. The spike in silver prices to highs not seen in decades also reflects speculative and volatile trading environments toward year-end.

Asian equity markets' outperformance, especially South Korea's KOSPI Index (+75.63%), was underpinned by a rebound in technology exports, robust corporate earnings, and policy stimuli supporting domestic growth. China's Shanghai Composite Index and Hong Kong's Hang Seng Index posted healthy gains above 18% and 27%, respectively, signaling investor optimism on Asia’s growth potential despite external pressures. Japan’s Nikkei 225 delivered a 26.18% return, benefiting from strong corporate profit outlooks and yen depreciation. European benchmarks including Germany’s DAX 30 and France's CAC 40 also gained over 10%, reflecting a broadly synchronized global economic recovery despite inflationary concerns.

US technology titans, including Alphabet, Microsoft, NVIDIA, and Tesla, collectively outpaced the broader market. NVIDIA's 38.91% return epitomizes the AI-driven investment boom. These gains were supported by improving earnings, accelerated adoption of AI-driven technologies, and favorable Federal Reserve policy shifts under the administration of U.S. President Donald Trump, who assumed office in January 2025. The administration’s cautiously moderated stance on trade policy and regulatory reforms bolstered market confidence after early-year turbulence caused by tariff threats.

Cryptocurrencies experienced a notable correction despite prior years of stellar gains and institutional support, including backing by U.S. President Trump. The declines in Bitcoin and Ethereum, over 6% and 10% respectively, suggest a market re-rating amid concerns over regulatory scrutiny, macroeconomic tightening prior to rate cuts, and competition from emerging digital assets and monetary policy uncertainties.

WTI Crude Oil’s 20.07% decline occurred despite geopolitical risks traditionally supportive of oil prices. The fall reflects persistent oversupply concerns, shifts toward renewable energy investments, and demand uncertainty due to slowing growth in major consumers. Simultaneously, the US dollar’s depreciation contributed to mixed commodity price dynamics, benefiting precious metals while dampening oil earnings in dollar terms.

Analyzing these disparate asset class performances points to several underlying trends. The flight towards precious metals and tech equities highlights investors’ dual search for growth and safety amid volatility. Strong Asia-Pacific equity performance underlines the strategic importance of emerging and developed Asian markets as engines of global growth. However, the setback in cryptocurrencies signals investor caution toward speculative and unregulated assets in volatile macroeconomic conditions. Commodities are undergoing structural shifts influenced by energy transition policies and supply chain realignments.

Looking ahead to 2026, these patterns suggest sustained opportunities and risks. Precious metals may maintain momentum if geopolitical tensions persist and inflation remains above target levels, keeping real yields low. Technology sectors, especially AI-focused companies, are poised for continued growth but face valuation scrutiny and potential regulatory challenges. Asian markets are expected to continue their ascent buoyed by domestic policy support and innovation-driven productivity gains. Conversely, cryptocurrencies could see further volatility shaped by regulatory developments and competitive innovations. Oil markets might remain pressured by energy transition trends and demand uncertainties.

Investors should incorporate diversified strategies balancing growth with hedging against volatility. Monitoring policy signals from central banks and geopolitical events will be crucial for navigating asset allocations. The interplay of monetary easing, fiscal stimulus, and technological advancement under U.S. President Trump's governance is shaping a complex but potentially rewarding investment landscape as the global economy enters 2026.