Within the first 20 days of the year, 80 banks have already exited the market. In December 2025 alone, 75 banks removed their nameplates from the branches. In just 50 days, a total of 155 banks disappeared.

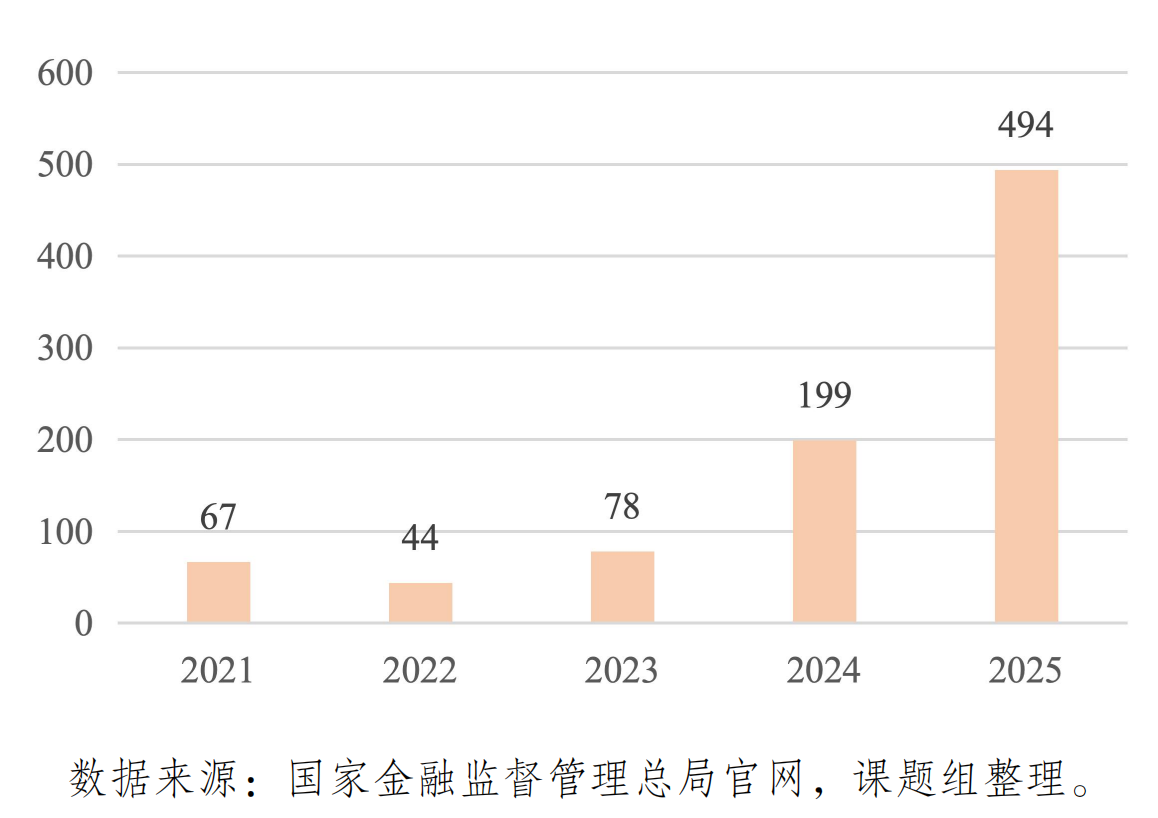

In recent years, the number of banks out of business has doubled year over year. In 2022, around 40 banks shut down; the number is about 80 in 2023; in 2024, the number surged to nearly 200; and by 2025, it is expected to approach 500.

As the number of small and medium-sized financial institutions rapidly declines, risks within these institutions are gradually being resolved. The wording at the Central Economic Work Conference has also evolved: in 2023, it was “coordinated mitigation of risks in small and medium-sized financial institutions”; in 2024, it became “prudently handling risks in local small and medium-sized financial institutions”; and the latest adjustment for 2025 is “deepening efforts to reduce quantity and improve quality among small and medium-sized financial institutions.”

It is worth noting that as the reform and restructuring of small and medium-sized banks continues, mergers and acquisitions have become a new option. There are increasing cases of mid- and large-sized banks acquiring village and township banks, converting small banks into branches or sub-branches of larger banks (known as “village-to-branch” or “village-to-sub-branch” transformations).

During this process, some new developments have emerged. When these mergers and acquisitions are put to a vote at shareholder meetings, some shareholders—especially many small and medium-sized shareholders—have cast dissenting votes. In some cases, up to 27.23% of small and medium-sized shareholders have opposed the deals.

New types and methods of mergers and acquisitions are also beginning to appear. For example, Bank of Guizhou recently disclosed that it will use a trust structure to acquire a village and township bank, marking the first time a trust has been used in the restructuring and reform of the banking sector. In addition, regional city commercial banks such as Bank of Jiangsu have achieved cross-provincial expansion by acquiring village and township banks in other regions.

Source: Report on the Development of Small and Medium-Sized Banks (2025)

Banks’ Shareholders Begin to Say "No"

The most recent case occurred on January 21, when Zhangjiagang Bank held its first extraordinary general meeting of shareholders in 2026 and approved the proposal on the merger and acquisition of Jiangsu Donghai Zhangnong Rural Bank, converting it into a branch. However, there was a split among shareholders: 4.42% of minority A-shareholders voted against the proposal.

A week earlier, on January 15, Sunong Bank held an extraordinary shareholders’ meeting and passed the proposal to acquire Jiangsu Zhangjiagang Yulong Rural Bank and establish it as a branch. Among all A-shareholders, 85.97% supported the proposal, 13.08% opposed, and 0.95% abstained.

Among minority shareholders holding less than 5%, the opposition rate was even higher: 80.25% agreed, 18.42% opposed, and 1.34% abstained.

A similar situation occurred at Guiyang Bank in November last year.

At its third extraordinary general meeting of shareholders in 2025, Guiyang Bank approved the proposal to acquire Xifeng Development Rural Bank and establish it as a branch. 80.83% of shareholders supported the proposal, 19.07% opposed, and 0.1% abstained. Among minority shareholders, 27.23% voted against.

Earlier, Guangzhou Rural Commercial Bank proposed to acquire Xingning Zhujiang Rural Bank, Heshan Zhujiang Rural Bank, and Shenzhen Pingshan Zhujiang Rural Bank, converting them into its own branches.

The voting results at the time showed that for the proposals to acquire Xingning Zhujiang Rural Bank and Heshan Zhujiang Rural Bank, 7.5% of votes were against and 1.63% abstained; for the proposal to acquire Shenzhen Pingshan Zhujiang Rural Bank, 7.5% were against and the abstention rate was as high as 9.22%.

Why Are Shareholders Voting Against?

On online platforms such as Eastmoney’s financial forums, minority shareholders have voiced specific concerns about listed banks acquiring rural banks.

For example, investors often worry about declining return on capital and dividend levels, since acquisitions require capital investment, which may dilute earnings per share and affect dividends. Many minority shareholders bluntly state that during the integration process, the high hidden costs of asset verification and risk disposal may leave the parent bank “spending money to buy trouble,” with little benefit in the short term and potentially increased bad debts and operational pressure.

From a performance perspective, most of the rural banks being acquired are under significant pressure.

Take the institutions that Guangzhou Rural Commercial Bank plans to absorb and merge as an example. Heshan Zhujiang Village Bank’s net profit in 2024 experienced a “halved” drop of about 50%, reaching only 15.37 million yuan, while its non-performing loan ratio rose to 2.19%. Meanwhile, the official websites of Xingning Zhujiang Village Bank and Shenzhen Pingshan Zhujiang Village Bank have not been updated for years; the former only recorded revenue of 51.03 million yuan in 2021, and the latter was previously penalized by regulators for internal control violations related to handling high-interest deposits.

In Guizhou, the village banks under Bank of Guizhou have also performed poorly. Its majority-owned subsidiary, Guangyuan Guishang Village Bank, posted a net loss of 8 million yuan in the first half of the year, while its minority-owned Huaxi Construction Village Bank achieved a profit of just 843,200 yuan in the same period.

Even in economically developed provinces such as Jiangsu, Zhangjiagang Yunnan Rural Commercial Village Bank’s net profit for the first ten months of 2025 was only 7.81 million yuan, a sharp decline from the full-year figure of 20.33 million yuan in 2024. Its total assets have also continued to shrink, dropping to 456 million yuan.

In addition to the acquisition targets under pressure, some acquirers themselves are also facing significant challenges. For example, Guangzhou Rural Commercial Bank’s third-quarter report shows that its operating income and net profit for the first three quarters of 2025 fell by 2.36% and 18.74% year-on-year, respectively. Since 2021, its revenue has been on a downward trajectory for four consecutive years. In 2024, revenue dropped by 12.79% year-on-year, and net profit decreased by 21.02%.

With its own profit growth momentum constrained, absorbing and merging these underperforming village banks will undoubtedly further burden its balance sheet.

Although Bank of Guizhou stated in its announcement that such moves are to “actively respond to national strategies and the latest policies, and enhance regional economic and financial service capabilities,” for minority shareholders, how to strike a balance between policy guidance and commercial interests remains a pressing challenge to resolve.

New Approaches in Acquisitions

Although opposition from some minority shareholders has not been enough to block acquisition proposals, more market-oriented and flexible approaches are gradually emerging. Small and medium-sized banks are beginning to seek breakthroughs in institutional design and operational boundaries during restructuring.

For example, in a recent case involving Bank of Guizhou, the bank announced that it would use a trust structure to acquire a village bank—marking the first time a trust has been used in banking sector restructuring and reform.

According to the deposit assumption agreement signed by both parties, from the date of assumption, Bank of Guizhou will take over the debts and related rights arising from the target deposits of Longli Guofeng Village Bank. As of the assumption date, the total principal and interest of the target deposits amounted to 1.913 billion yuan. After deducting the relevant rights and interests inherited by Longli Guofeng Village Bank along with the debts, the consideration for this assumption is 1.849 billion yuan.

Analyzing its mechanism, the essence of this model is that Bank of Guizhou assumes the creditor’s rights formed by the deposits, in exchange for the trust beneficiary shares established by Longli Guofeng Village Bank based on the future cash flow-generating asset income rights. This structure isolates risks—potential non-performing assets or operational risks of the village bank will not directly affect the core balance sheet of Bank of Guizhou, but are instead buffered through the trust structure.

A banking industry analyst said that this model has three advantages: the trust mechanism bundles dispersed assets, simplifying the complicated process of individual verification and settlement; the independence of trust assets shields them from liquidation disputes of the original village bank, thus safeguarding the rights and interests of the assuming party; and neither party uses cash in the transaction, reducing Bank of Guizhou’s short-term capital occupation and capital consumption.

Against the backdrop of widespread concerns among minority shareholders over “dilution of returns,” this represents an institutional exploration aimed at balancing the efficiency of risk resolution with the protection of shareholder interests.

In another case, Jiangsu Bank, a local city commercial bank, achieved cross-regional expansion by acquiring a village bank in another province.

Specifically, Jiangsu Bank acquired 100% equity of Ningbo Jiangbei Fumin Village Bank and converted it into the Ningbo Branch, marking the first time a city commercial bank has expanded across provinces in this way. Unlike the traditional approach of internal absorption by the main sponsor, this case to some extent breaks the regulatory restrictions on cross-regional operations for city commercial banks, seizing the window of opportunity for reform.

The target of this transaction—Ningbo Jiangbei Fumin Village Bank—was established in 2011 and was wholly owned by Shengjing Bank. According to information disclosed by the Shenyang United Assets and Equity Exchange, on February 21, 2025, Shengjing Bank officially listed all 100 million shares of the bank for transfer, with a reserve price of 120 million yuan. Although the village bank’s performance has been lackluster, with losses of 2.1585 million yuan in 2023 and 688,000 yuan in the first eleven months of 2024, and total assets of only about 204 million yuan, its core value lies in providing Jiangsu Bank with the qualification for cross-regional development, enabling it to break through its original geographic limitations and establish a directly managed branch in the economically developed Ningbo market.

For city and rural commercial banks, the path to expanding into other regions and increasing branch networks has been completely shut off in recent years. By acquiring village and township banks in other areas, Bank of Jiangsu has extended its business reach deep into the territory of its long-time rival, Bank of Ningbo. (Author|Cai Pengcheng, Editor|Liu Yangxue)

South Korea’s Stock Market Capitalization Tops Germany’s at $3.25 Trillion

South Korea’s Stock Market Capitalization Tops Germany’s at $3.25 Trillion